Free Invoice Templates (500+) PDF, Word, XLS

(No Ratings Yet)

Invoice Maker offers a complete library of 100% free downloadable invoice templates in Word, PDF, and XLS formats, no credit card or signup required. If you are looking to make one-off invoices, start by using one of our hundreds of templates. For an overview of how to use blank invoice templates, visit our How To Create Invoices guide.

Our invoice templates are organized by category for easy navigation. They are 100% free to use, no credit card required, no email address required for instant download. For a listing of all 500+ Invoice Templates, go here

Invoice Templates By Category (15)

How to use an Invoice Template

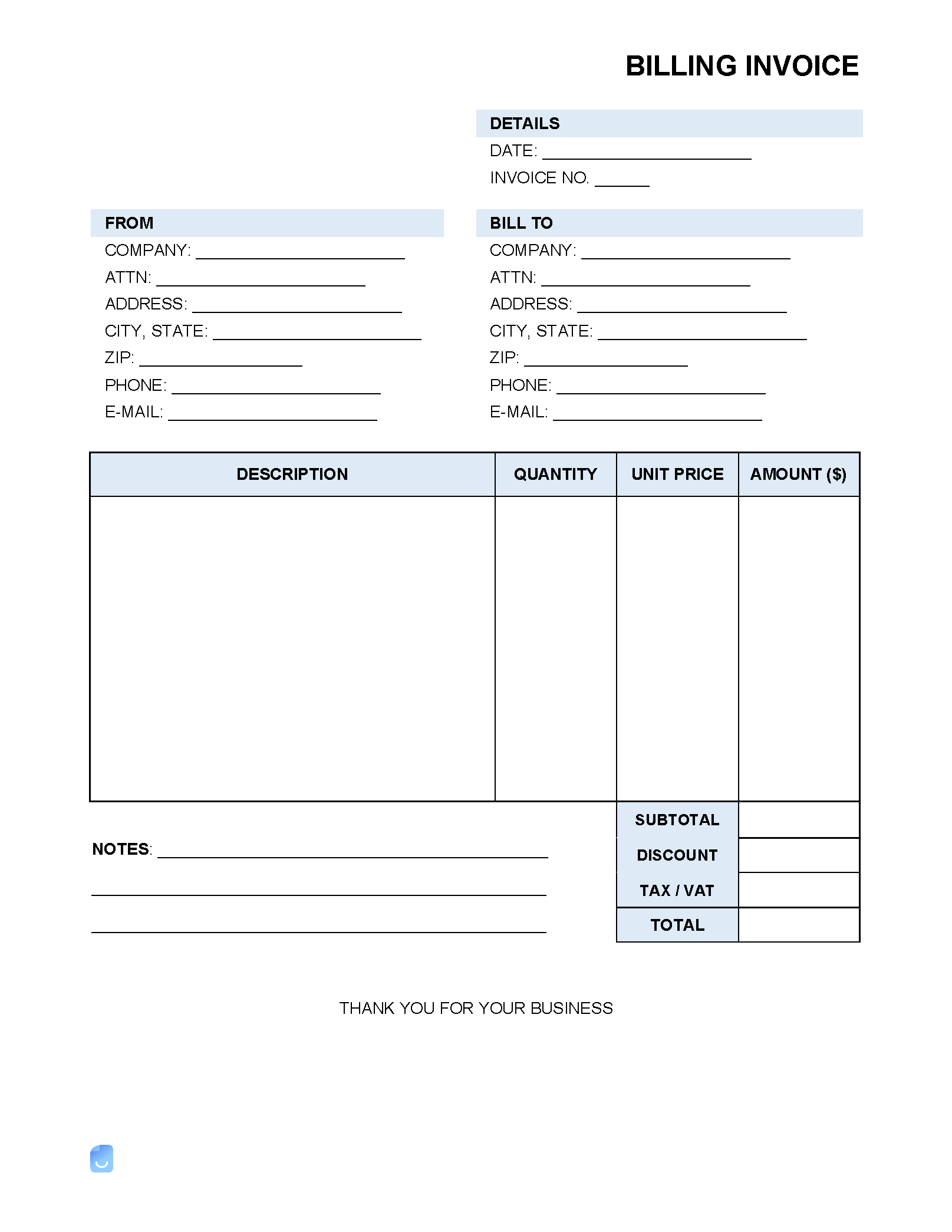

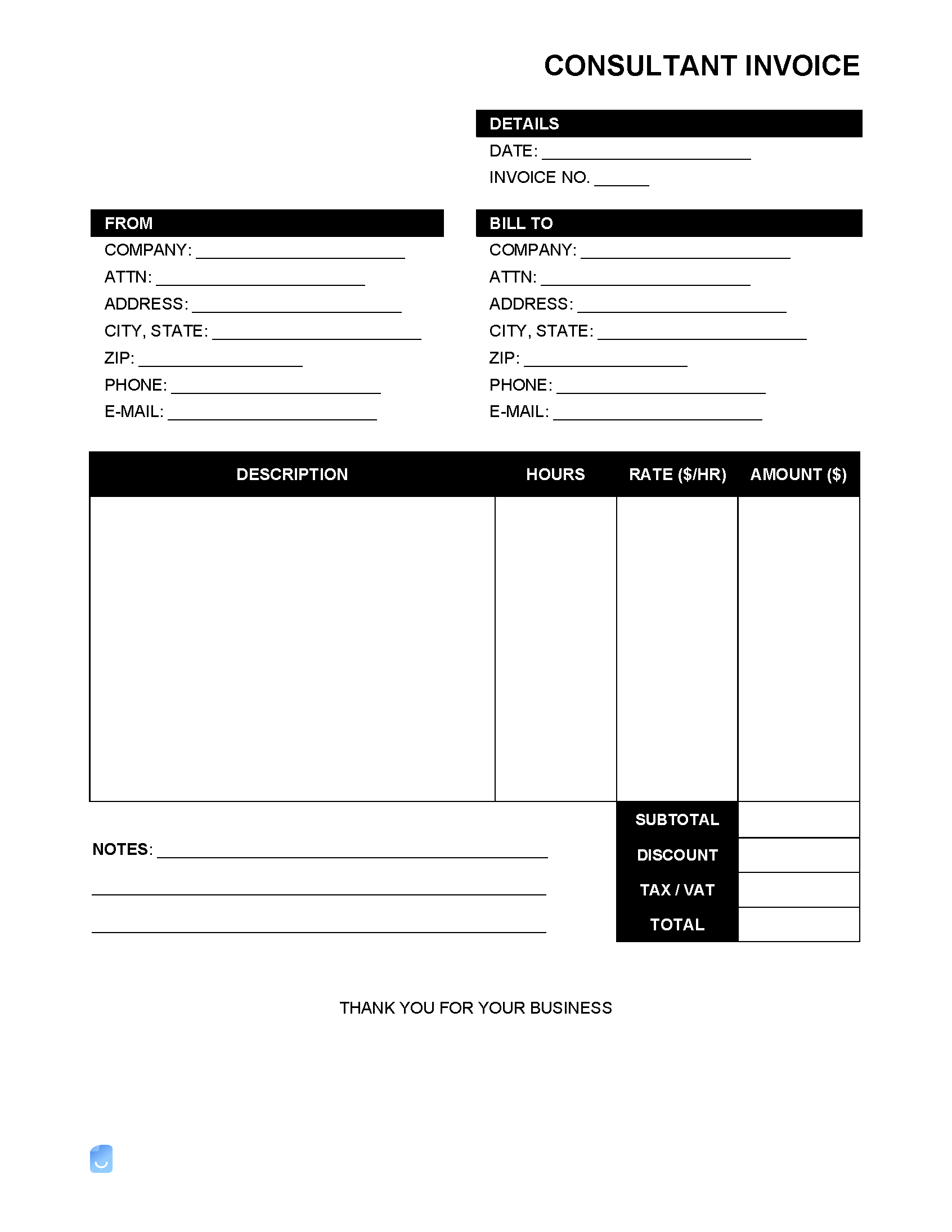

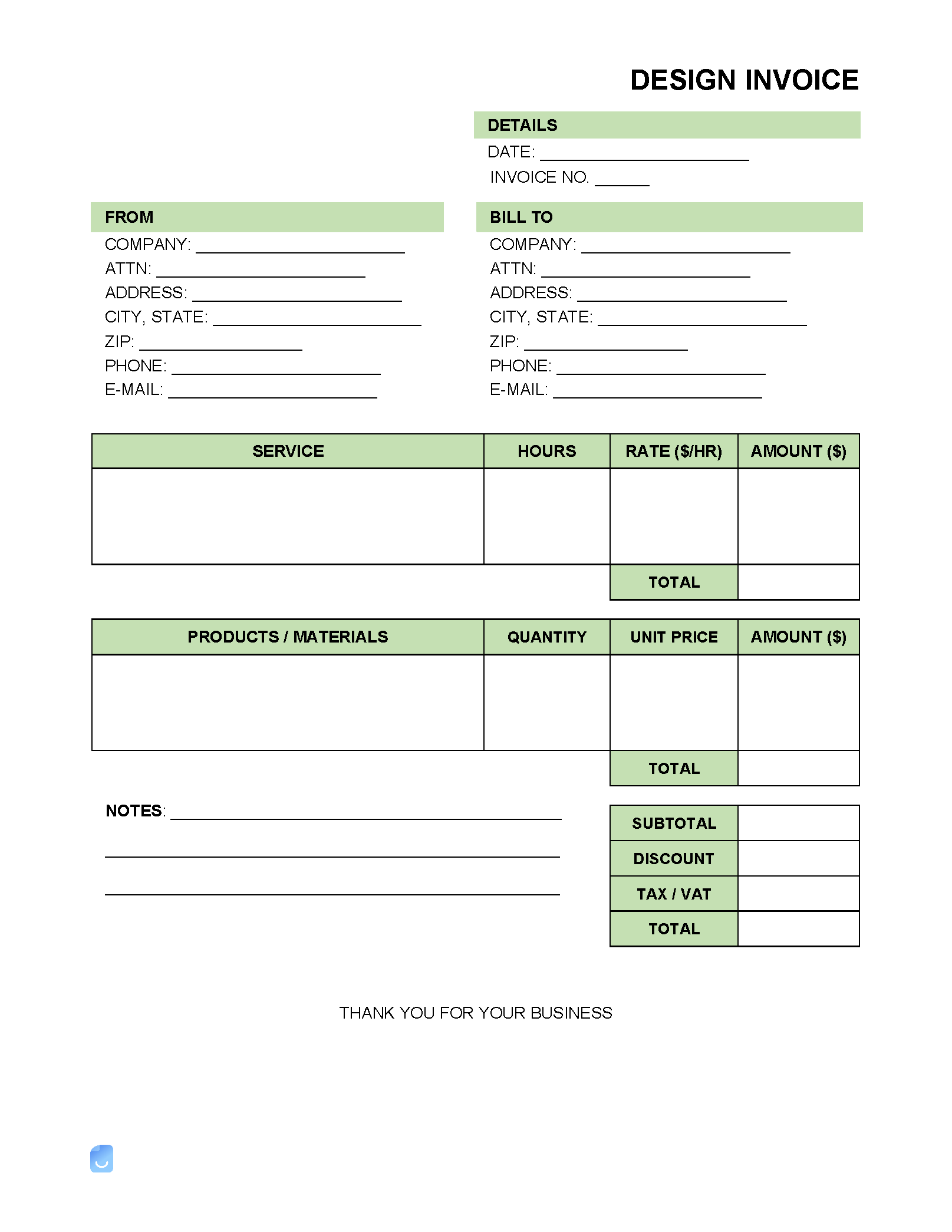

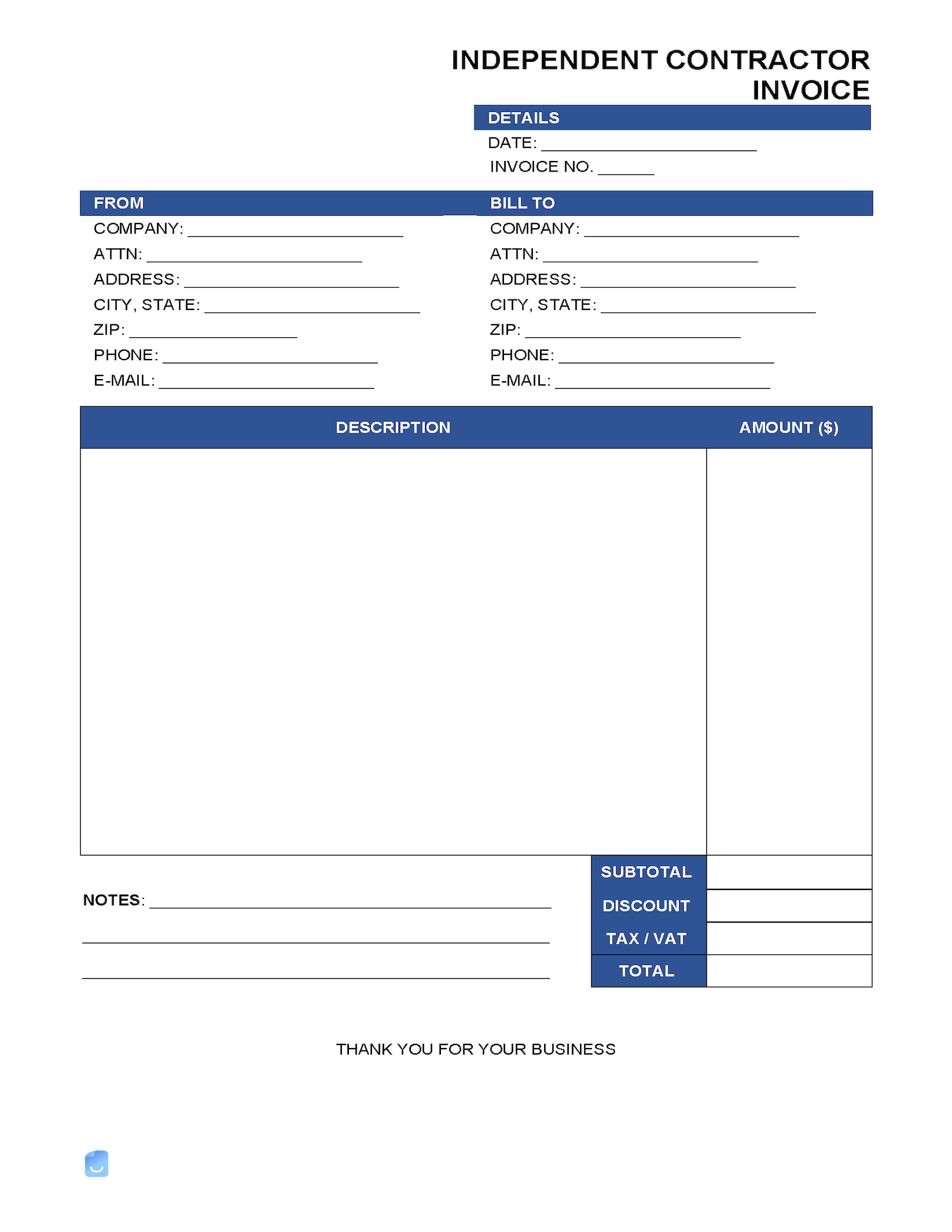

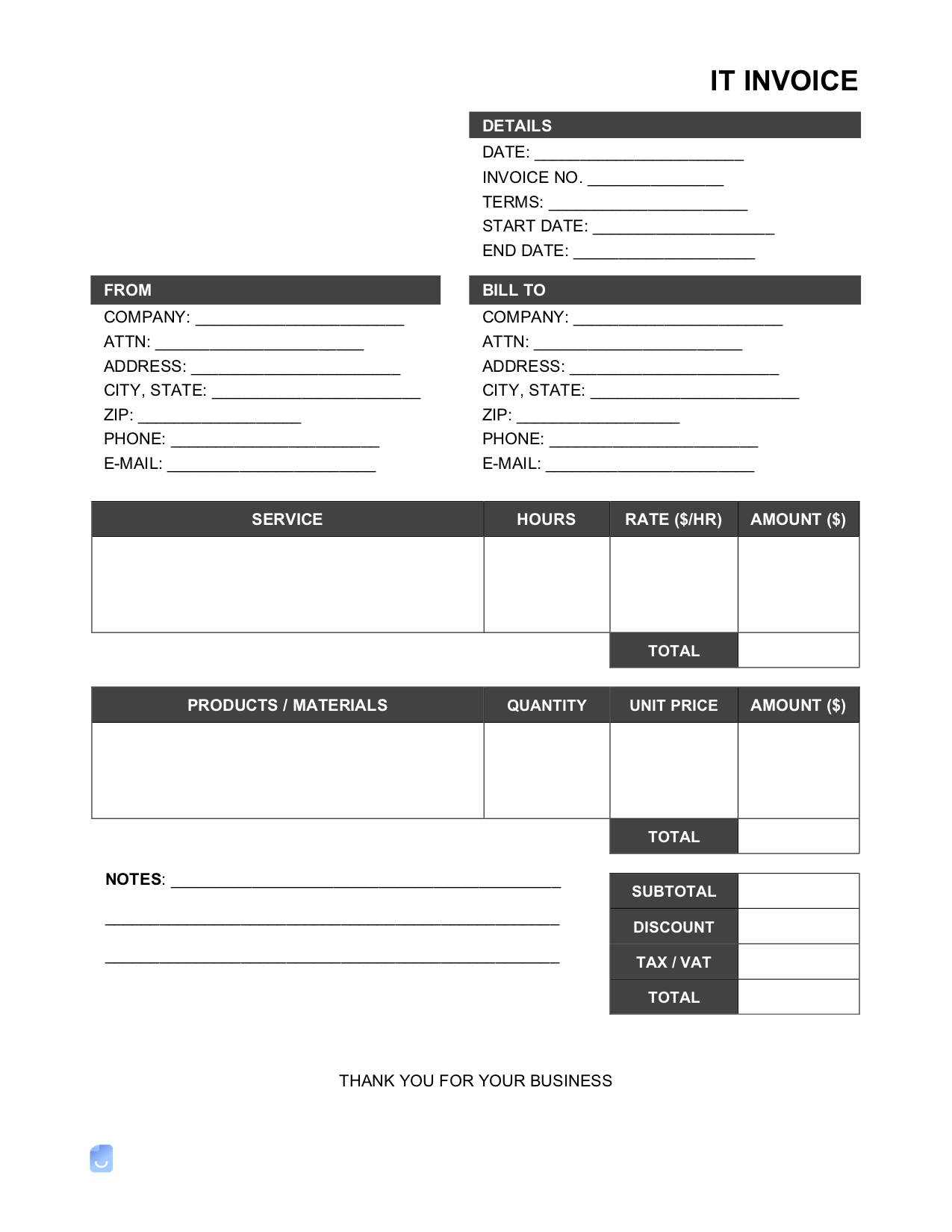

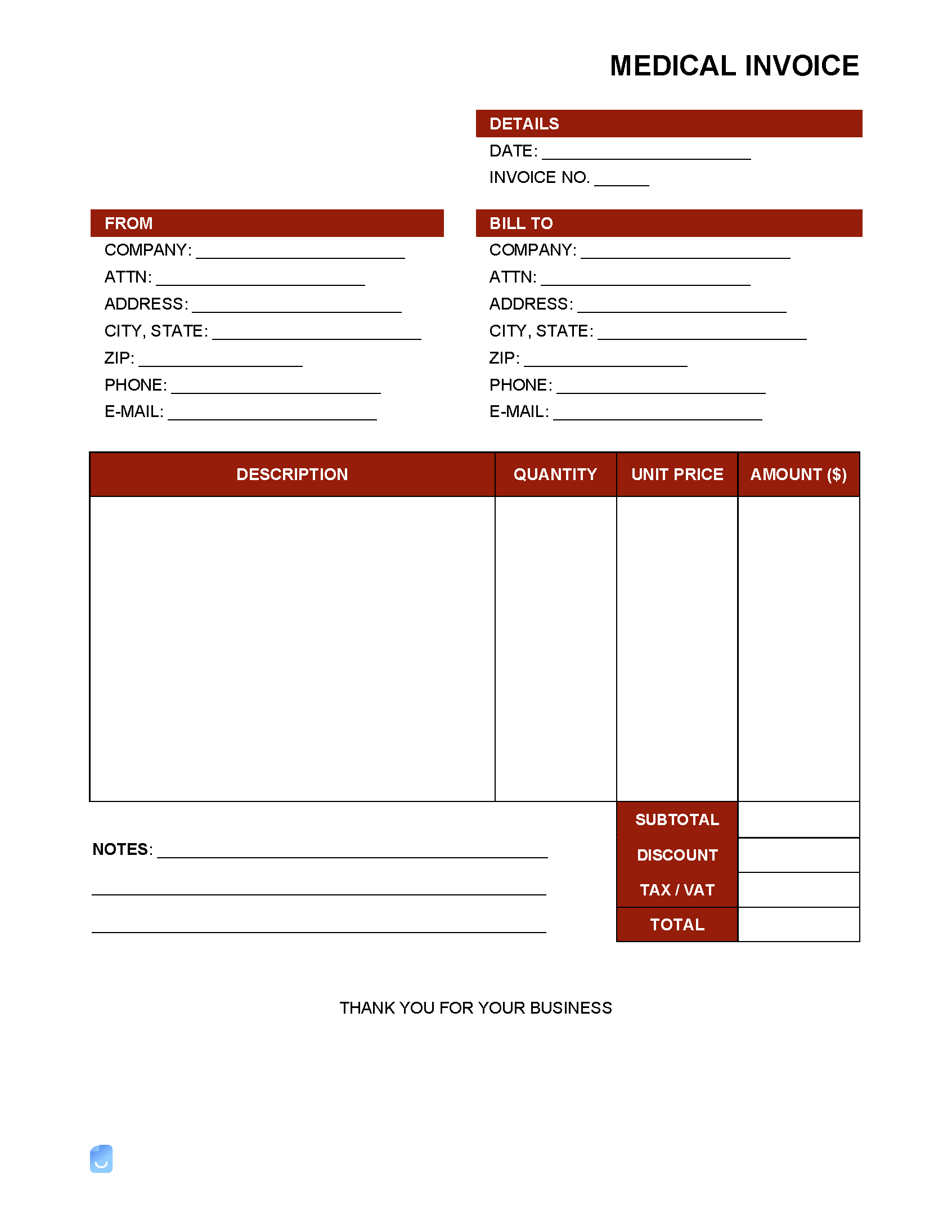

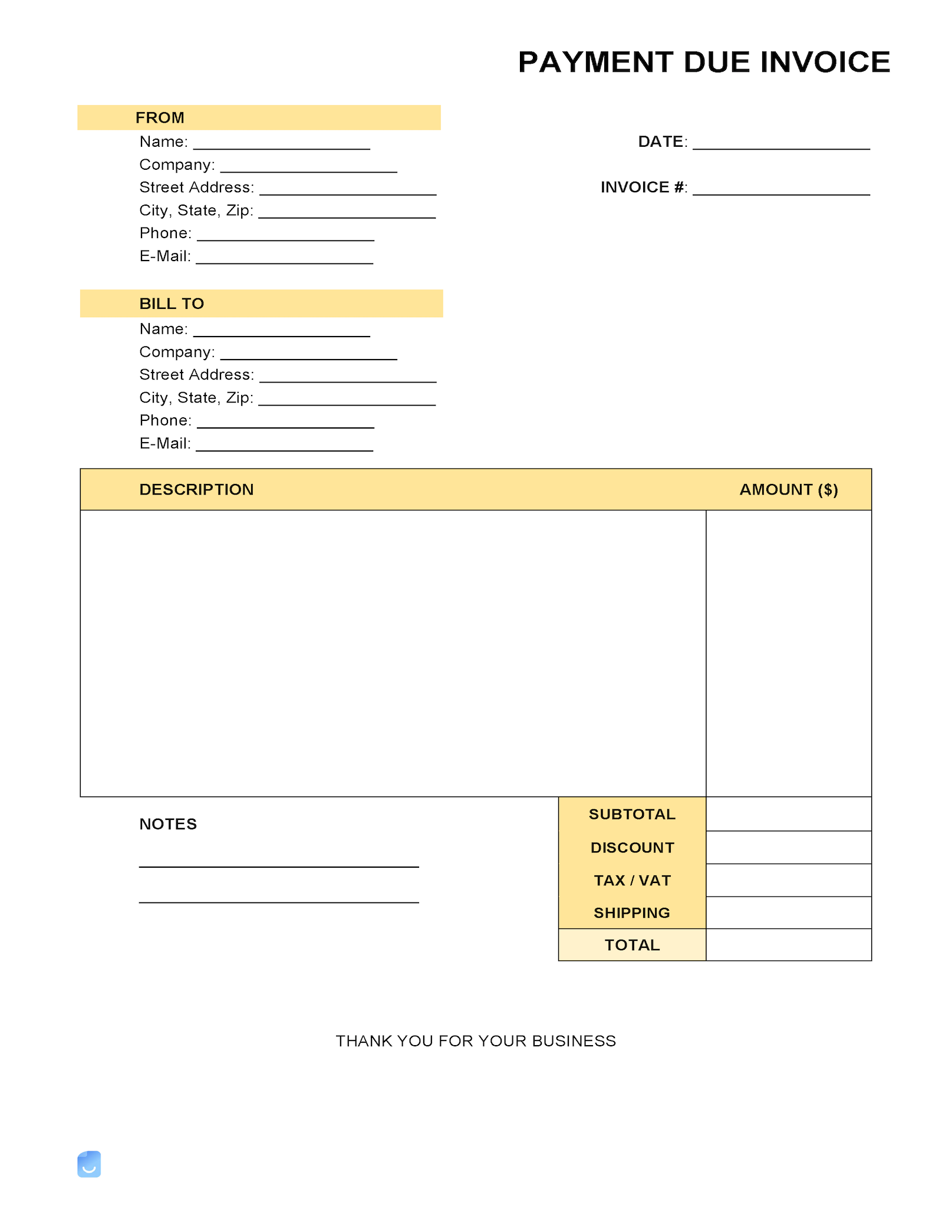

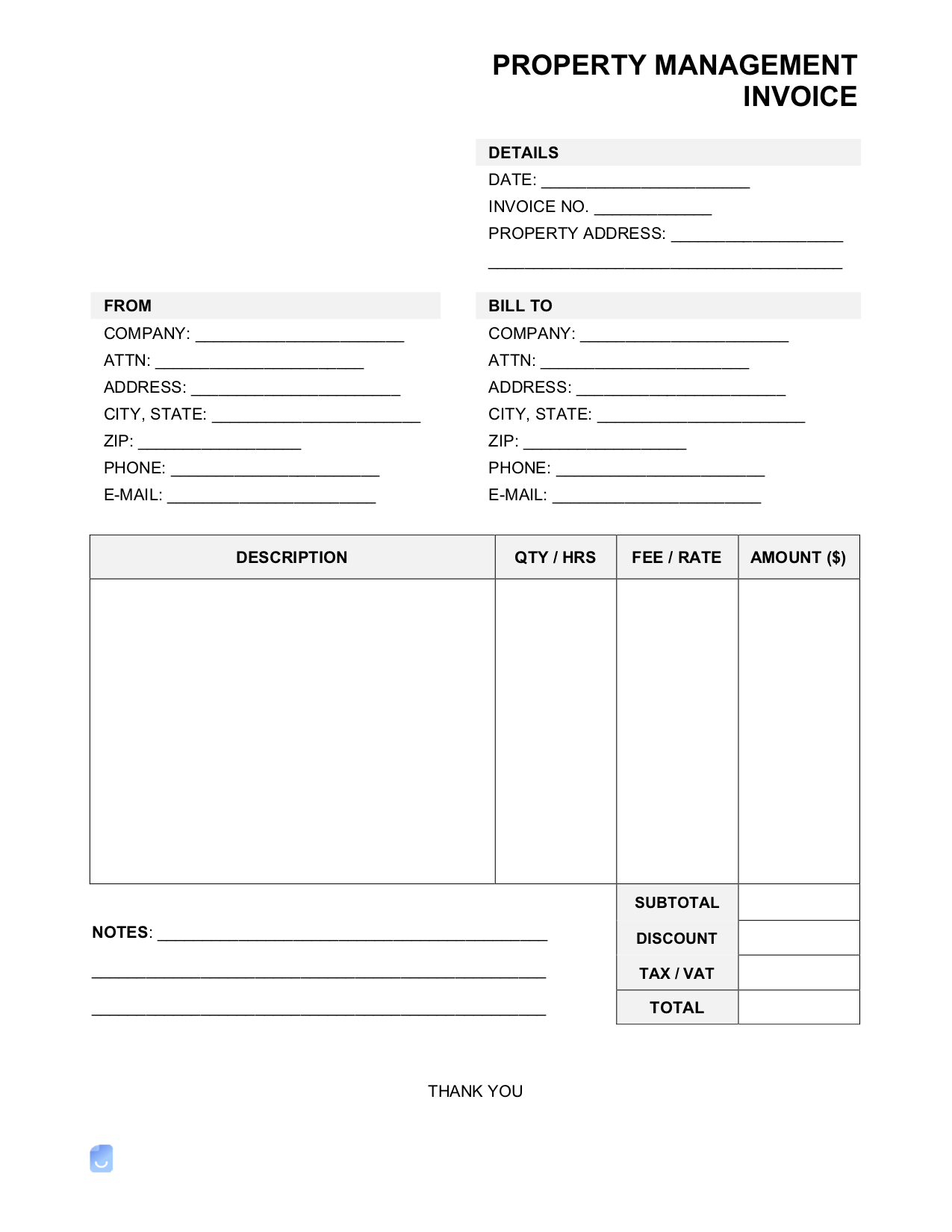

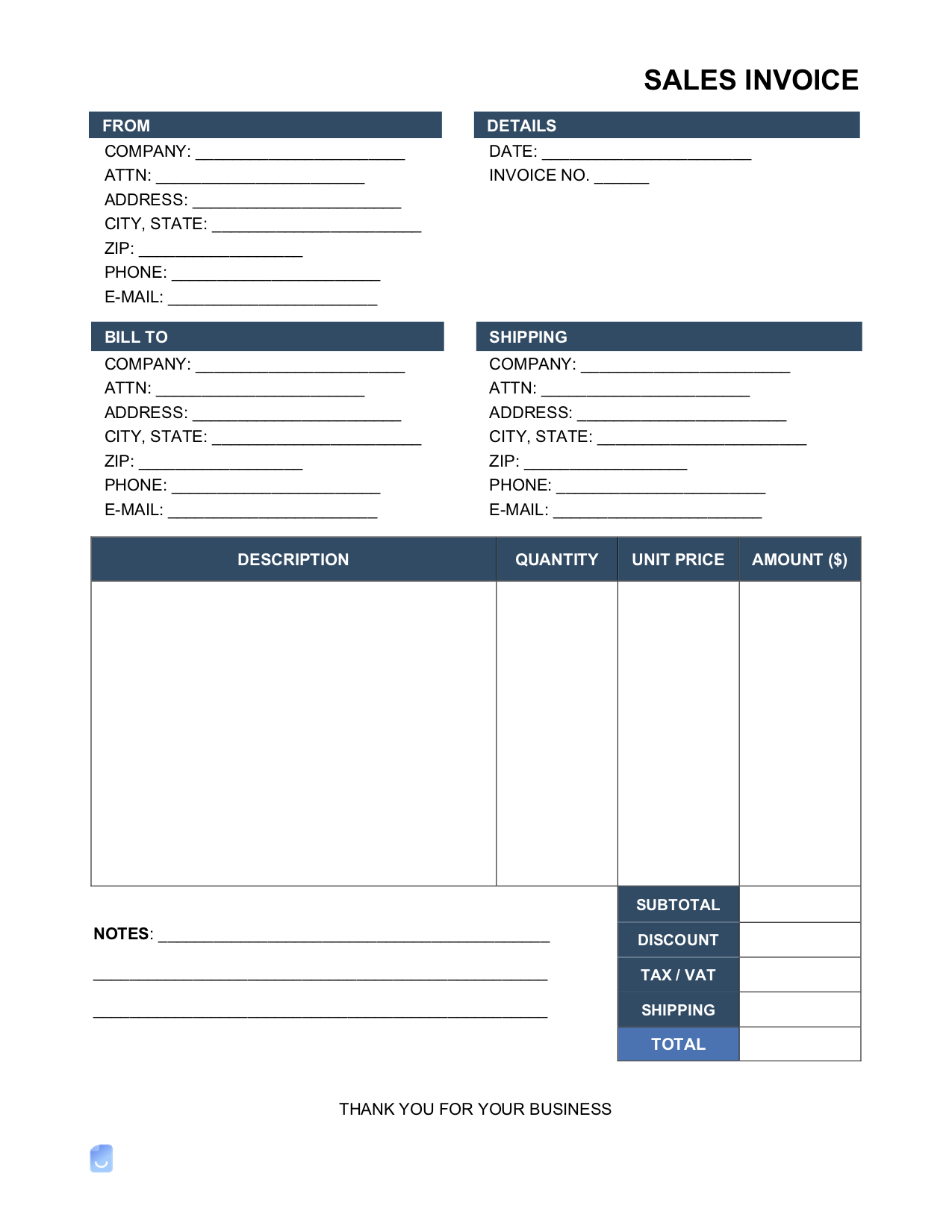

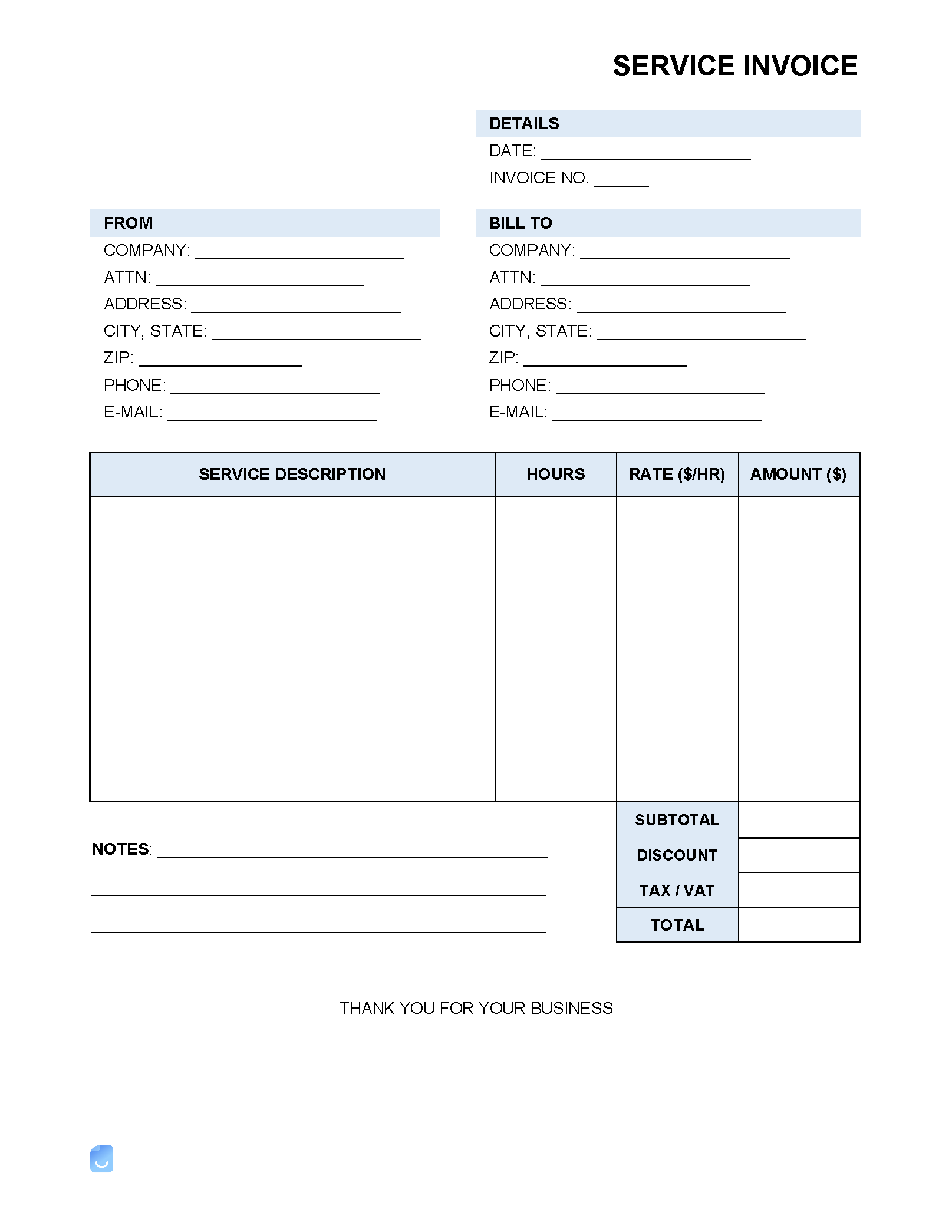

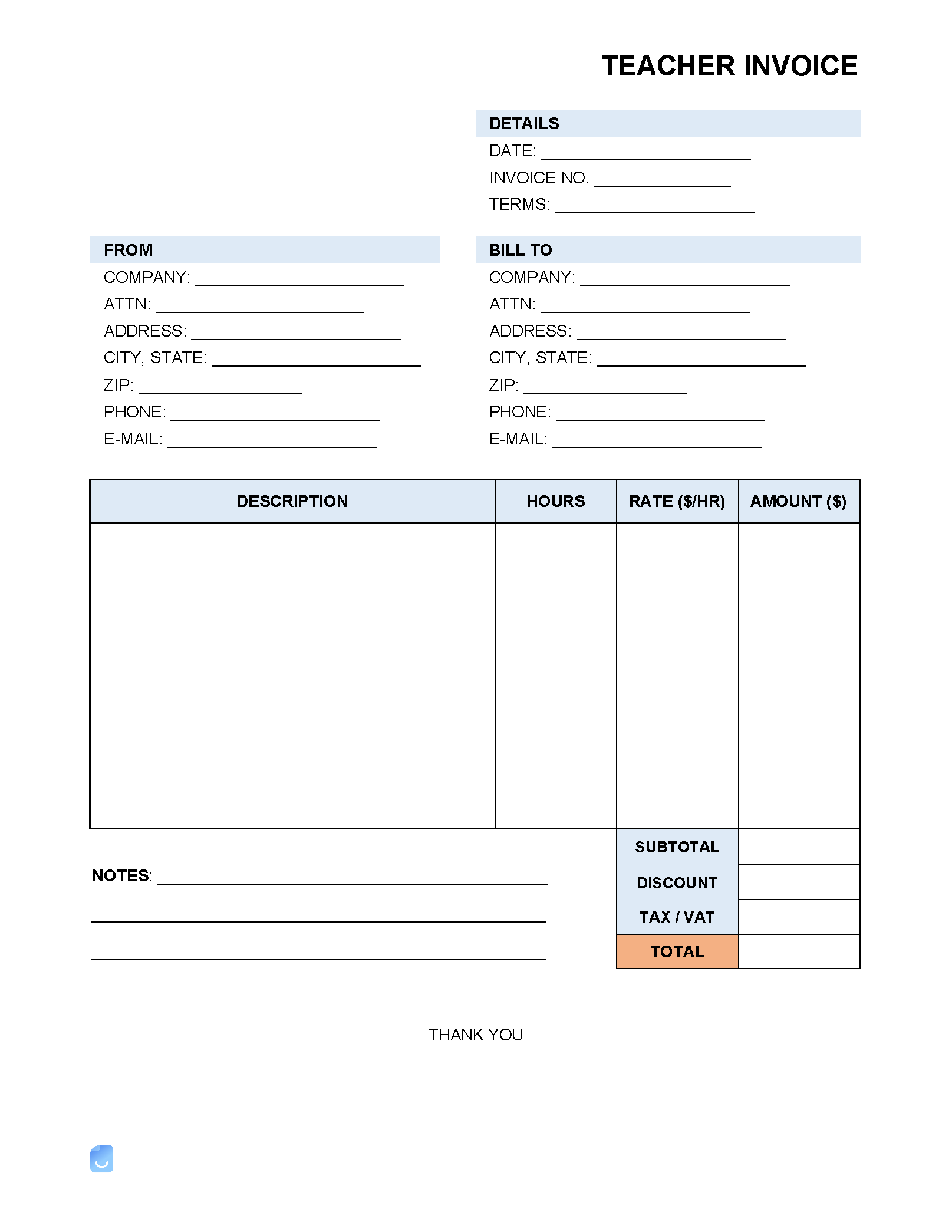

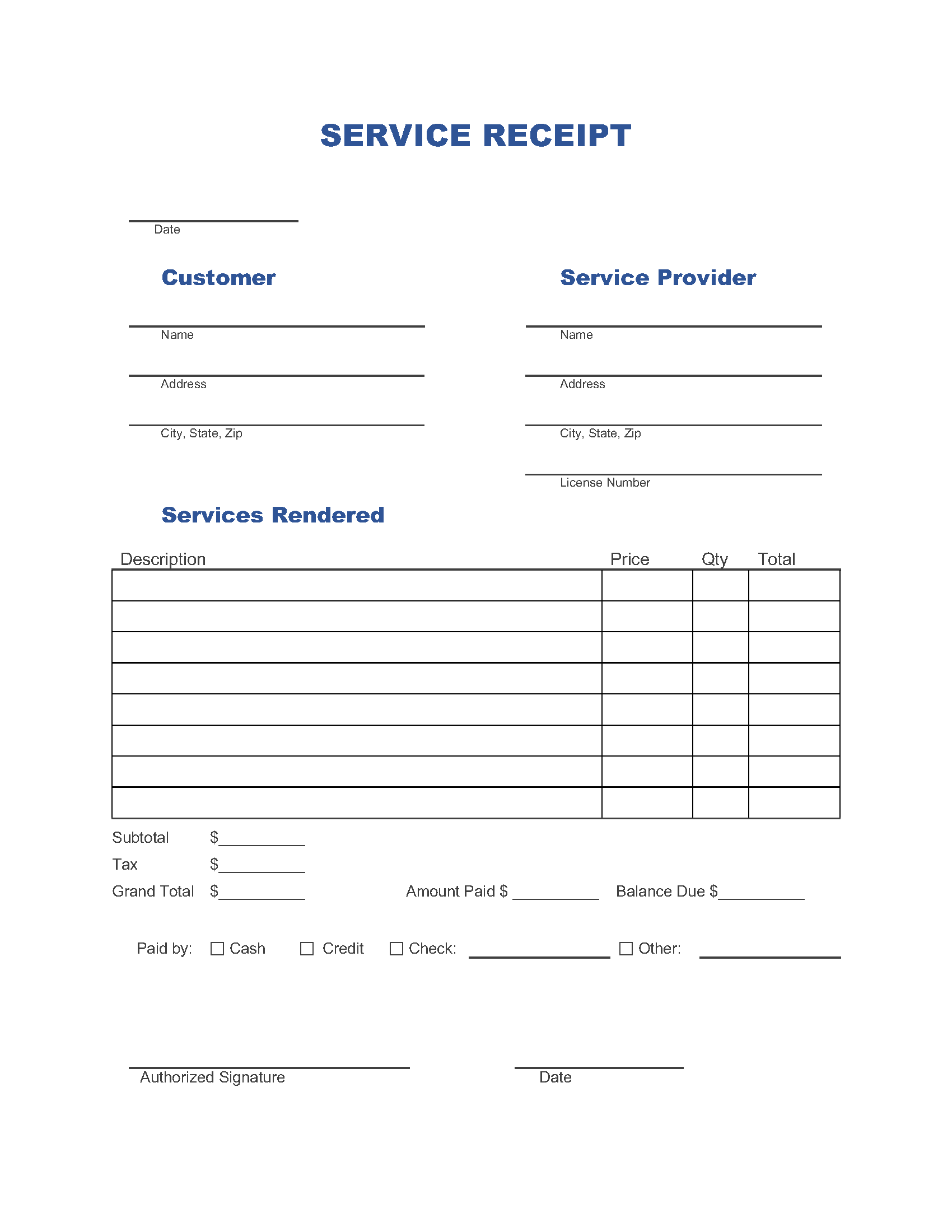

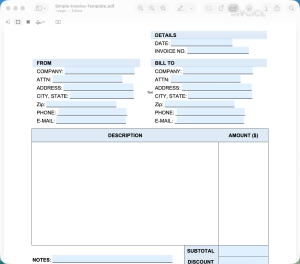

When using an invoice template, start with your business details. That means your name, address, contact info, and your logo if you have one. This ensures that you first add your name, logo (if you have one), address, and contact information so every invoice is clearly linked to your business. Give each invoice a unique number, include the date you sent it, and set a clear due date so there’s no confusion. List what you’re charging for in a simple, itemized way. Include descriptions, quantities, rates, and totals, and don’t forget to add any taxes or discounts if they apply. Make sure to specify payment terms, such as net 15 or net 30, and let the client know what payment methods you accept. If you charge late fees or have any notes, include them too. Once you’ve filled everything out, double-check it for mistakes, save a copy for your records, and send it off right away. Staying organized with your invoices helps keep your cash flow steady and avoids headaches down the road.

Invoice Generator vs. Invoice Templates

Invoice templates are pre-designed documents that can be downloaded and customized to the user’s needs. A third-party app, such as a PDF editor or word processor, is required to edit the fields manually.

An invoice generator is a software tool that streamlines this process by creating a custom invoice based on user input. The fields are automatically populated with data the user is prompted to enter, saving time and reducing errors in the process.

One important benefit of using an online invoice generator is direct integration with payment processing platforms. This allows the recipient to immediately pay the invoice according to options offered by the seller, such as credit card, ACH transfer, or digital wallets. If you want to professionalize your invoicing process, use our free generator.

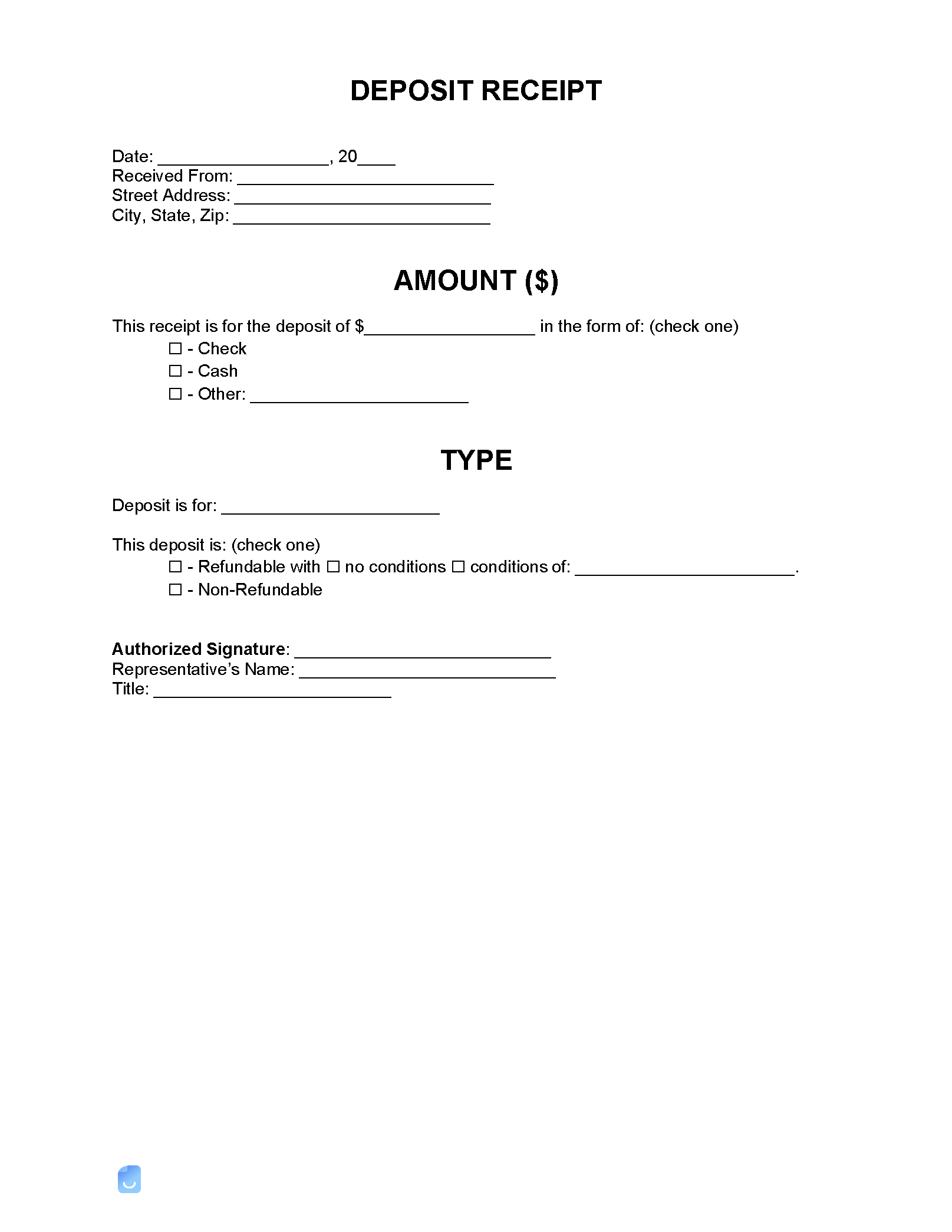

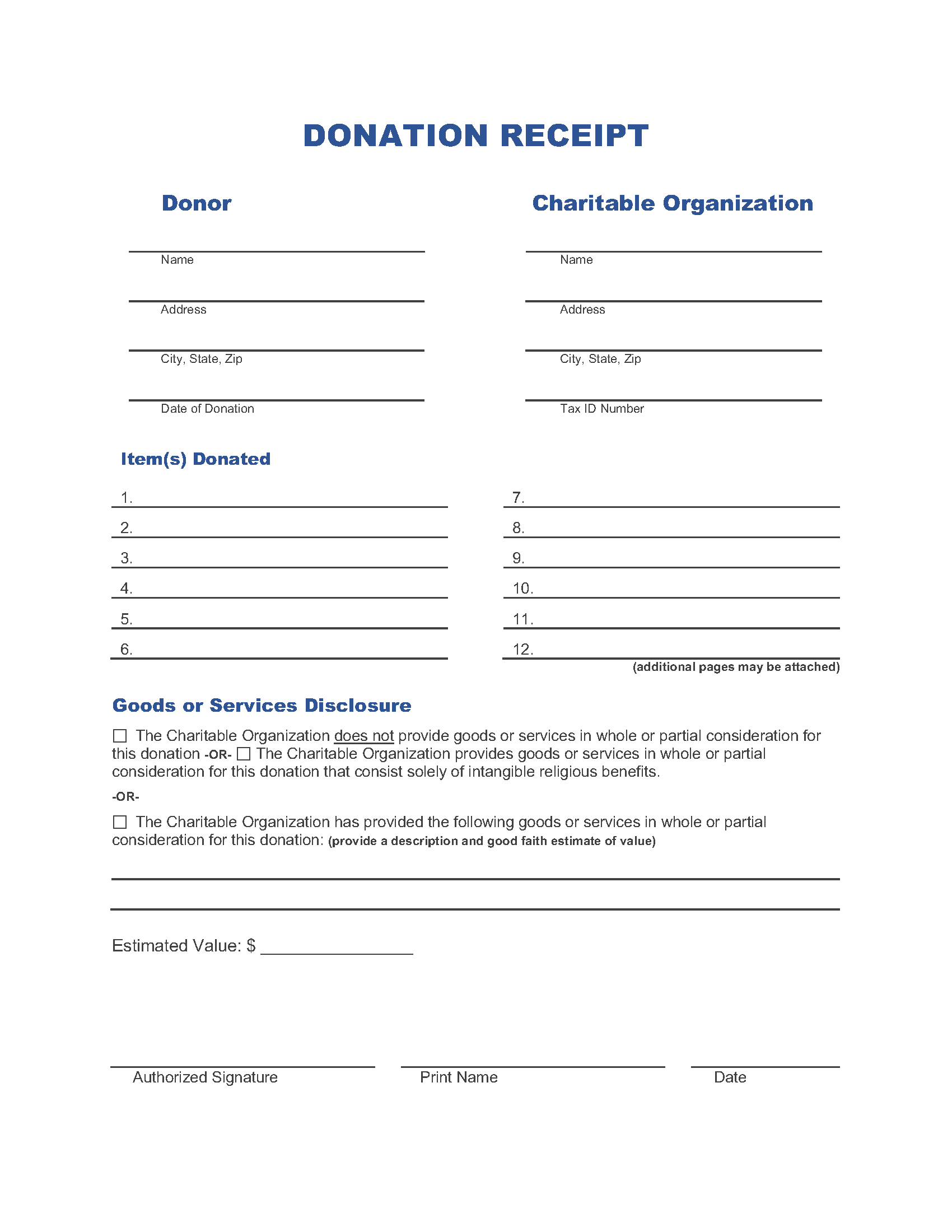

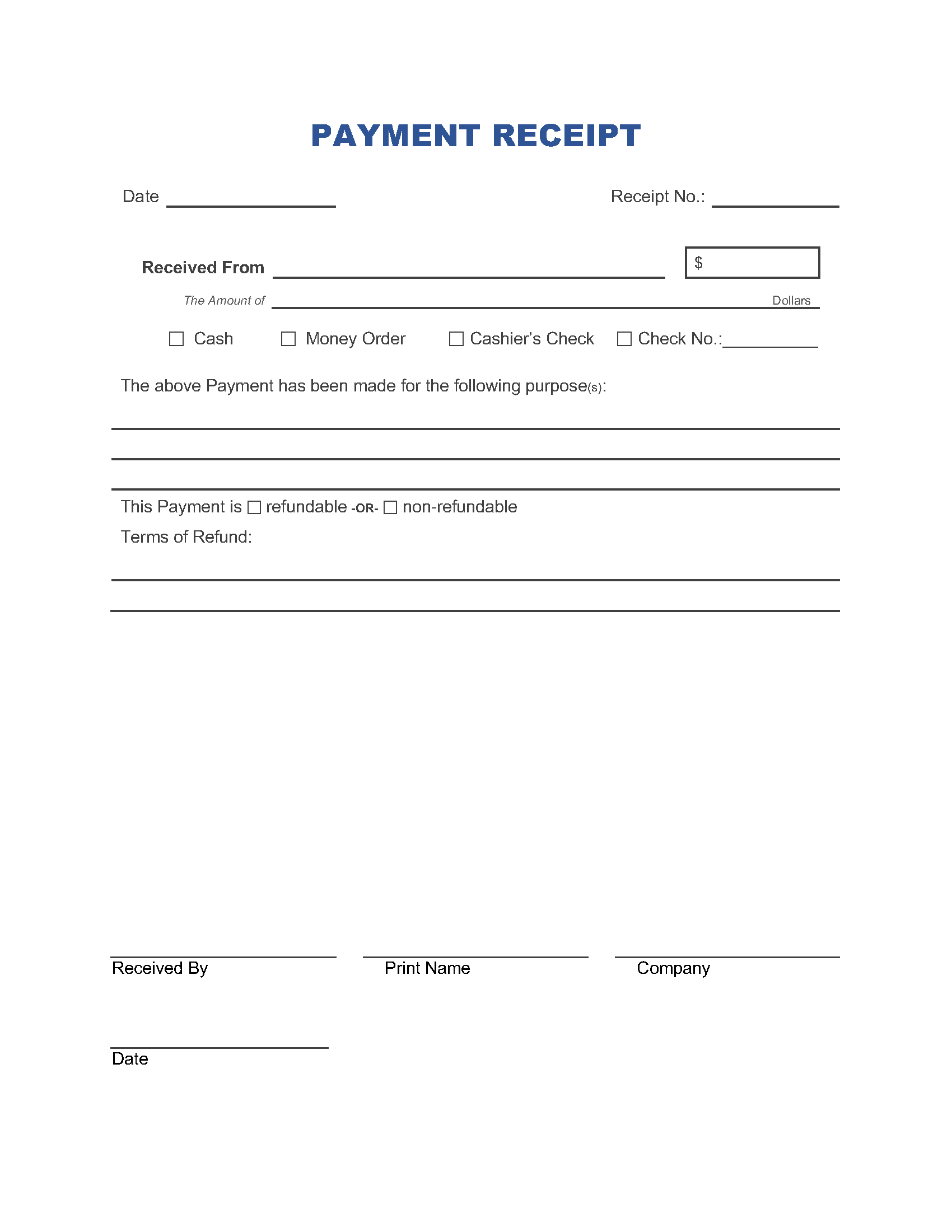

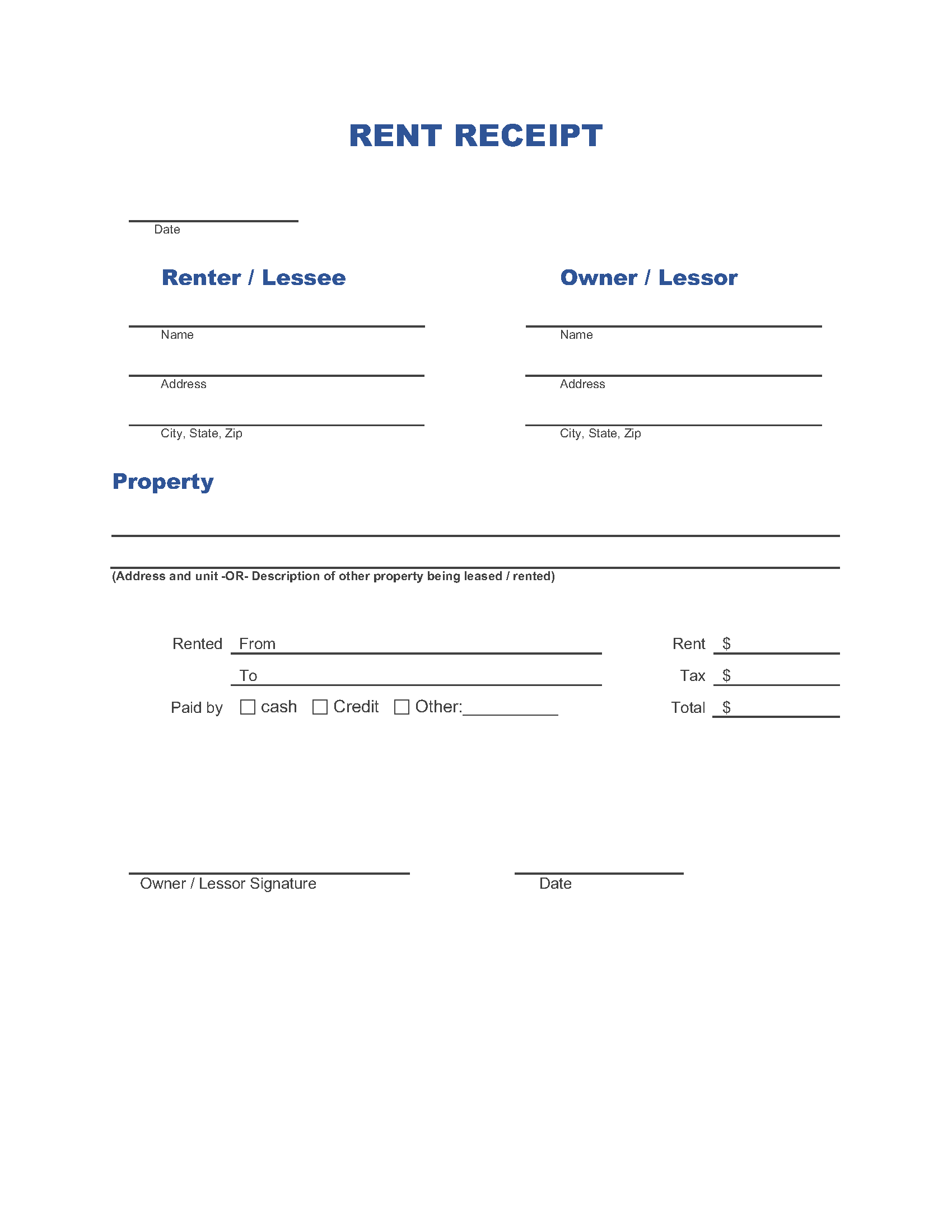

Invoice vs Receipt

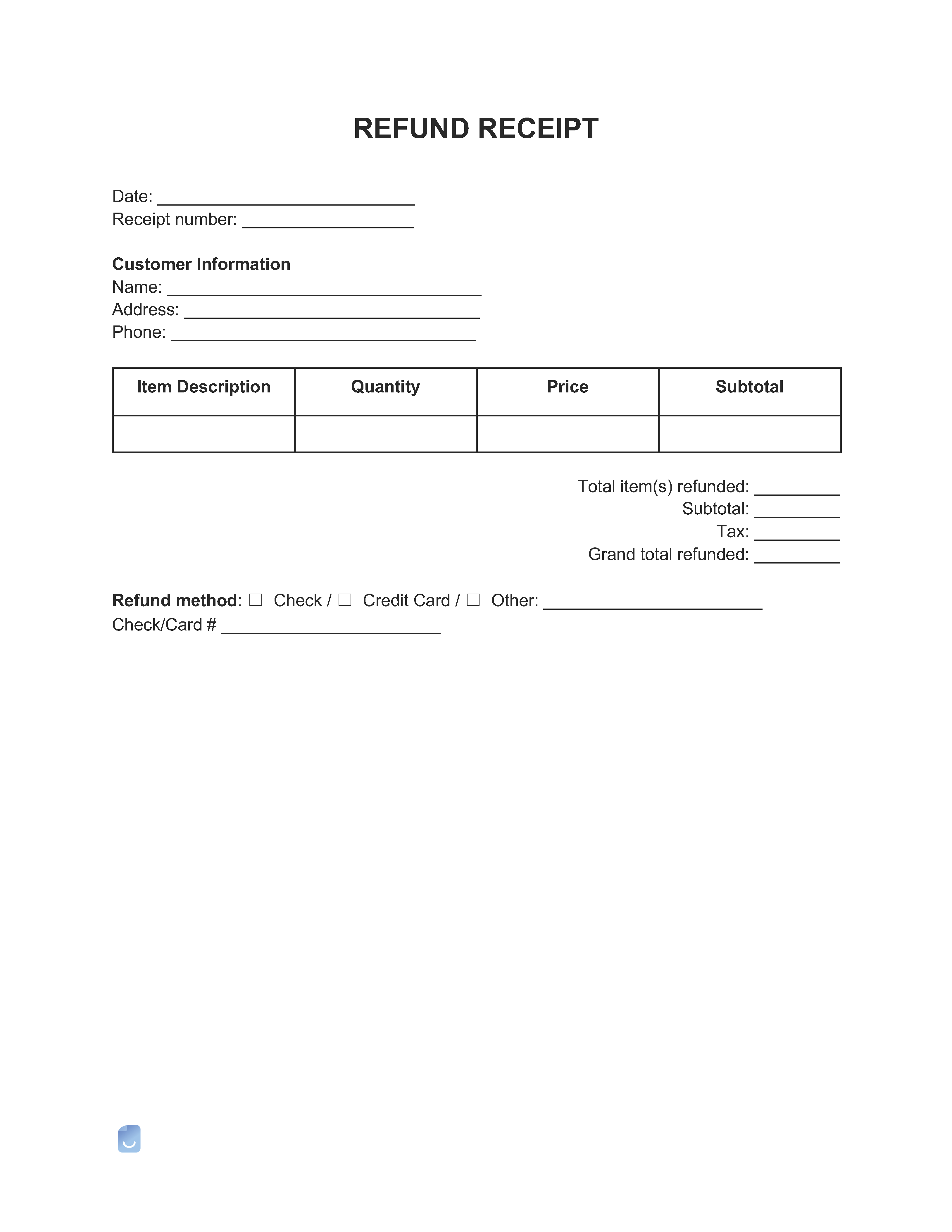

Invoices and receipts are similar but exactly the same, and it’s important for freelancers or small business owners to know the difference. An invoice tells someone what they owe you. You send it before you get paid, and it should include what the payment is for, the amount due, and when you expect payment. A receipt comes after you’ve been paid. It’s proof that your tenant or customer has paid. I always send invoices first to keep a clear record of what’s owed, then issue a receipt once I receive payment. This helps keep things organized and prevents confusion or disputes later.

How to make an Invoice (7 steps)

Step-by-step instructions for creating an invoice from a template using our library. For a complete guide on how to make an invoice in other formats or using applications, or what to include on an invoice user our free guide “How to make invoices”

Step 1 – Search for a template

Step 2. Select a format (Word, Excel, PDF, or Google Docs)

Step 3. Download to your computer or mobile device

Step 4. Open the saved invoice from your device

Step 5. Fill in the invoice details

Step 6. Save the invoice

Step 7. Send the invoice to the client for payment

Send the invoice to the client via email, text message, mail, or hand deliver it to them to request payment.

By Type (500+)

Browse our full library of more than 500 free invoice templates. Listed below alphabetically.

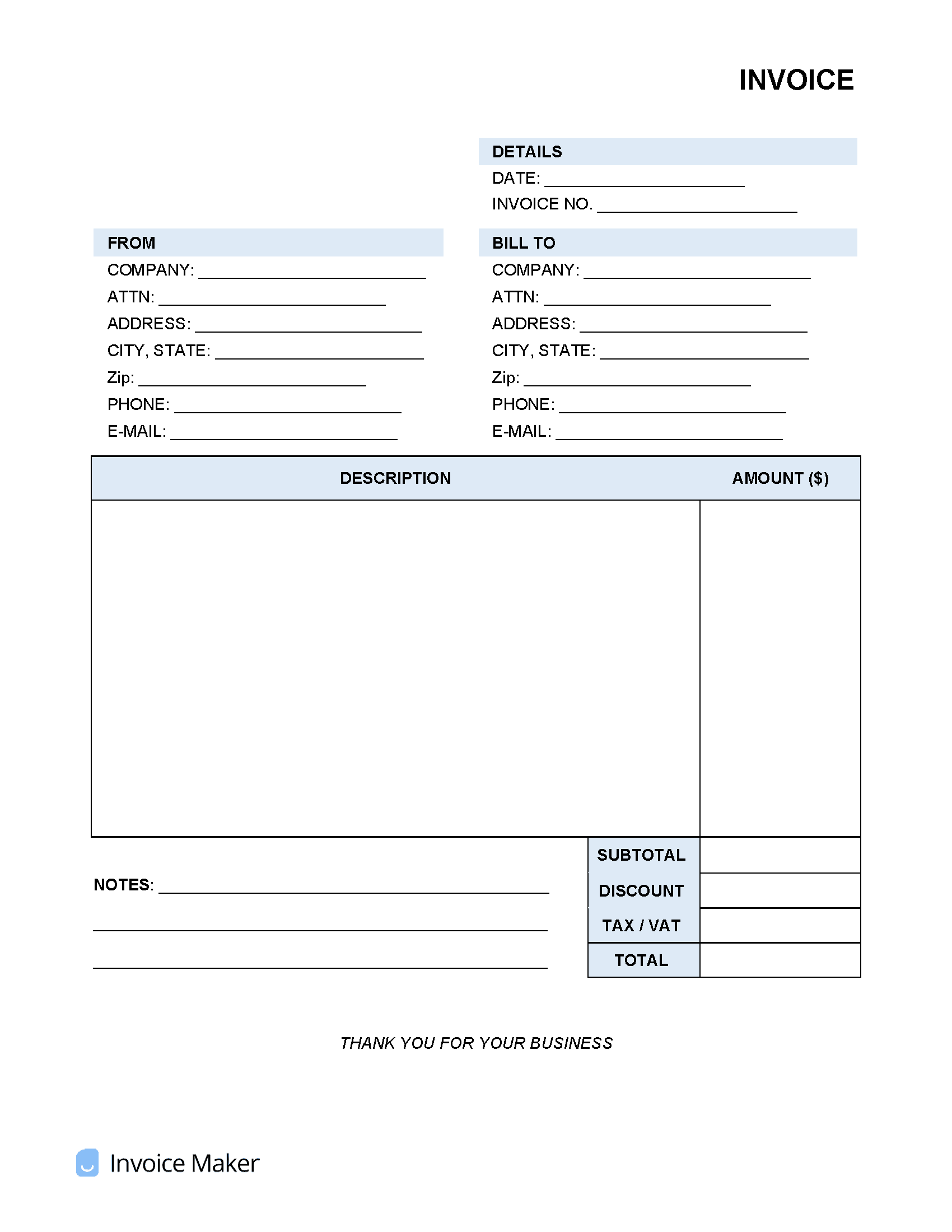

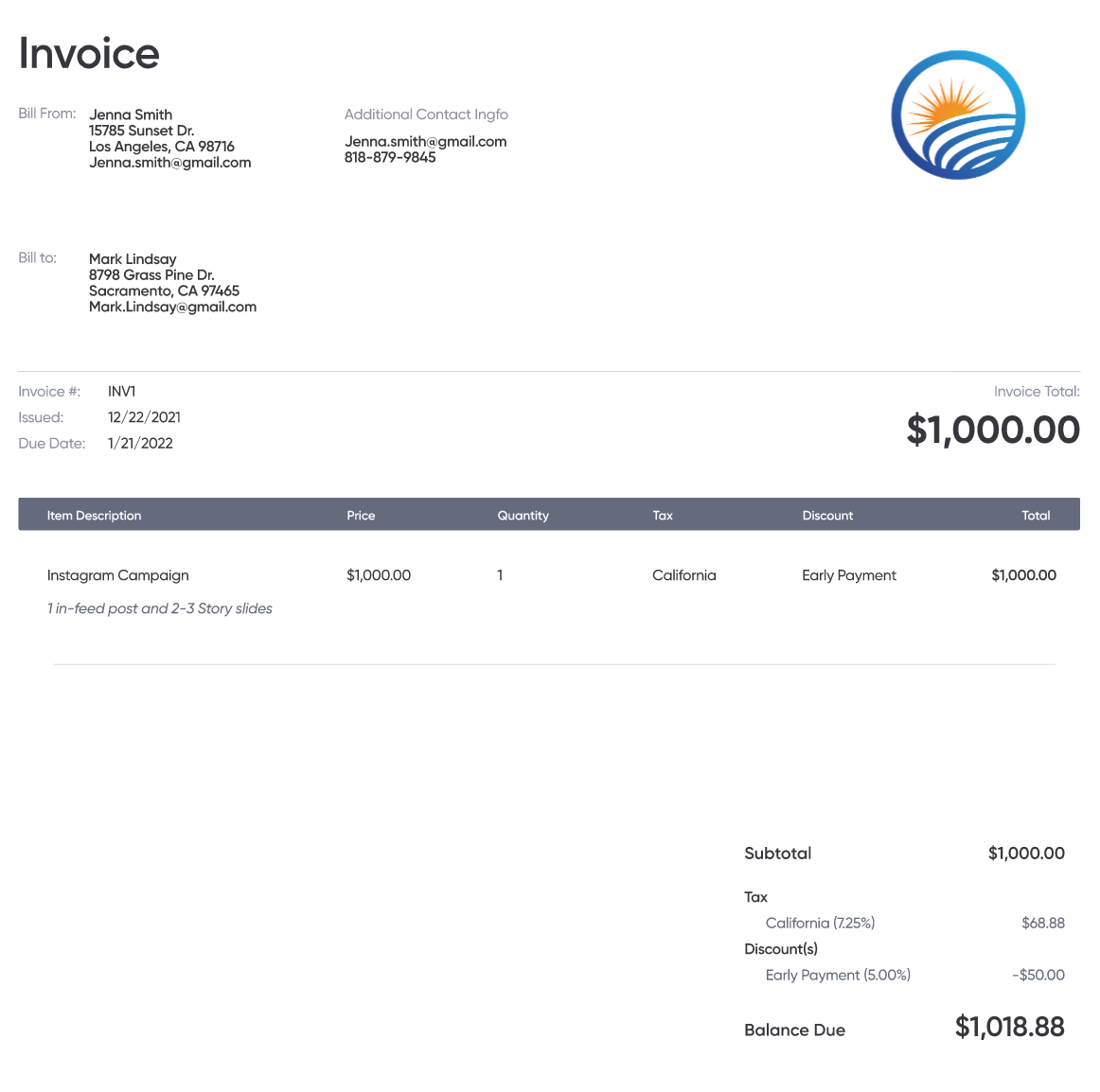

Sample Invoice

Not sure where to start? Learn the basics in our complete guide on how to create invoices before customizing your template.

Sample

FAQs

Simply download our free template. Open it in Microsoft word, excel or a pdf editor. Fill it out and save it

Yes. 100% free downloadable invoice templates by use available in Word, PDF, and XLS formats. Simply download the template you need and use it completely free

Yes, you are welcome to edit the templates for any use you see fit

Yes, you can use the template as many times as you want.

If you need to track invoices, payments and status software like invoicemaker.com may be a better fit. if you need a simple one-off invoice a template is likely fine.

We offer more than 500 invoice templates by type, service, format completely free. Browse our gallery to find anything you need.